[ad_1]

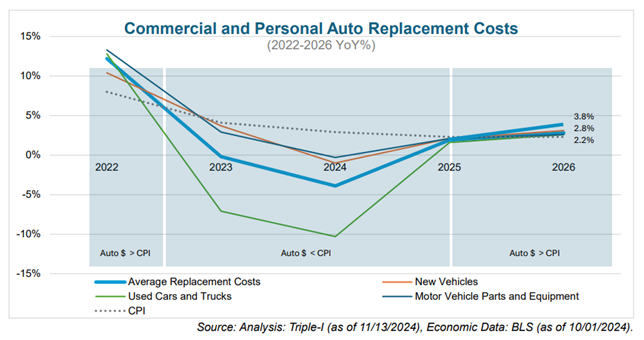

Triple-I expects the pace of increase in average property/casualty insurance replacement costs to exceed increases in the consumer price index in 2025 and beyond as auto replacement costs rise for the first time since 2022 and CPI continues to decline.

Triple-I’s replacement cost index for personal and commercial auto tracks changes in the price of vehicles, parts, and equipment that make up the replacement costs facing insurance carriers providing collision insurance for both personal and commercial motor vehicles. These costs – which have increased by as much as 30 percent over the past five years – are expected to increase by 2.8 percent in 2025.

The index combines replacement costs data for motor vehicles by age and for parts and equipment from the CPI for All Urban Consumers. These cost drivers were chosen from a wider selection of U.S. government sources, including the Bureau of Labor Statistics, Bureau of Economic Analysis, Federal Reserve, Census Bureau, and the Departments of Labor, Transportation, and Energy.

“While we expect the economic drivers of P/C insurance performance to continue improving 2025, performance will be constrained by replacement cost increases, rising natural catastrophe losses, and geopolitical uncertainty,” said Triple-I Chief Economist Dr. Michel Léonard.

[ad_2]

Source link

{kind=link}